African fintechs are no longer experimenting with cryptocurrencies; they are building them into the region’s financial plumbing. From Nairobi to Lagos and Cape Town, startups are embedding stablecoins and blockchain rails into cross-border payments, remittances, and merchant settlements.

Increased crypto adoption can also be linked with customers increasingly seeking faster transfers, cheaper fees, and payment methods that work around the clock. However, this opportunity comes with a challenge of oversight, putting pressure on regulators to write and rewrite rules, instead of observing from the sidelines.

This shift changes the perspective for fintech founders and cross-border startups: Crypto can unlock scale, but only for businesses that are ready to do it safely. Understanding compliance requirements is crucial to foster trust and navigate risks.

This article offers a detailed guide to the crypto regulatory framework for African fintechs. It breaks down the regulatory environment, explores best practices, and highlights strategies to navigate an evolving sector while staying ahead of compliance risks.

At YoguPay, we believe compliance can make or break fintech innovation. That’s why we prioritize a compliance-first approach, building payments infrastructure that meets global regulatory standards without compromising efficiency or customer experience.

Africa’s Crypto Moment in Numbers

Cryptocurrency adoption is not just hype. Chainalysis data shows Sub-Saharan Africa received $117 billion in on-chain value between July 2022 and June 2023, making it one of the fastest-growing regions for crypto activity. Nigeria alone ranked second globally for grassroots adoption in 2024, with nearly $59 billion in crypto inflows in a single year.

Why? African consumers and businesses face pain points that crypto directly solves. Sending $200 to Africa costs an average of 8.45%, almost triple the global average, according to World Bank data. Stablecoins and crypto rails are providing faster and cheaper alternatives, especially when paired with mobile money networks that already process $1.4 trillion annually across the continent.

But with scale comes scrutiny. The same networks that move family remittances also move illicit flows. Regulators, once cautious observers, are now enforcing licensing, Know Your Customer (KYC) rules, and cross-border data-sharing requirements.

Key Compliance Considerations for Fintechs

For fintechs to thrive within Africa’s crypto space, adherence to compliance is not optional but strategic:

- Understand Local Regulations: Fintechs must map country-specific crypto laws and compliance mandates such as licensing, classification of crypto assets, and AML/KYC/ KYB obligations. Early engagement with regulators through sandboxes fosters clearer understanding and cooperation.

-

- Implement Robust AML/CFT Controls: African regulators emphasize AML and CFT compliance given risks around fraud and illicit financing. Accurate customer identification, transaction monitoring, and reporting suspicious activities are pillars of compliance.

-

- Leverage Regulatory Technology: Tech-enabled compliance tools that automate KYC processes, transactional analysis, and reporting significantly reduce manual overhead and enhance regulatory transparency. Adopting these technologies supports operating in multiple jurisdictions with varying rules.

-

- Prepare for Emerging Regulations: Fintechs should stay alert to impending regulatory shifts, such as digital asset tax policies, advertising restrictions, and CBDC rollouts, adapting business models accordingly to maintain compliance and competitiveness.

-

- Regional Cooperation and Harmonization: Participating in fintech associations and industry groups can help advocate for harmonized crypto regulations across borders, reducing complexity and fostering greater market trust.

At YoguPay, our advantage lies in embedding compliance into every layer of product development, from KYC/AML checks to transaction monitoring. We ensure fintechs can scale with confidence and access opportunities across multiple markets.

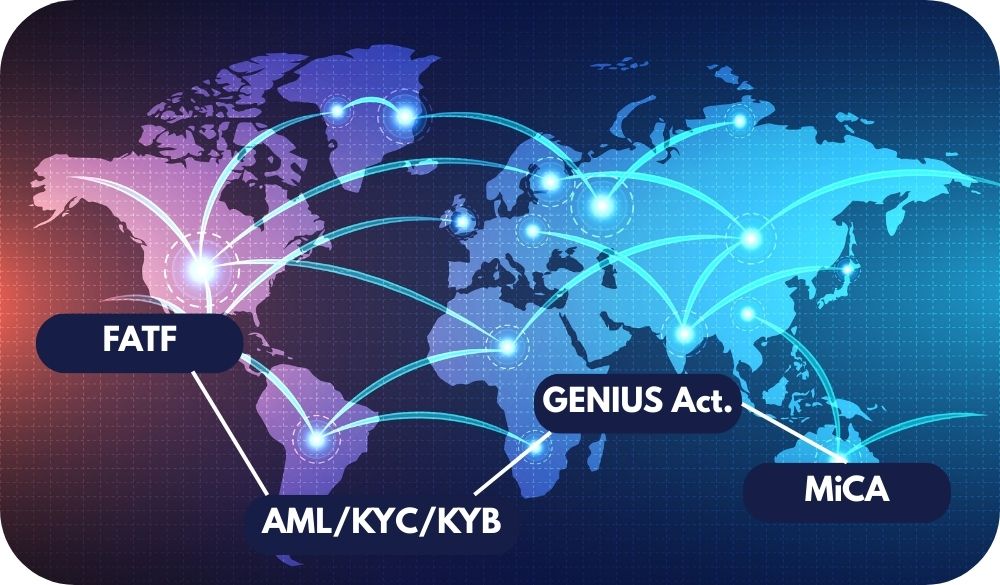

The Global Rules That Set the Tone

For African fintechs eyeing cross-border growth, crypto compliance isn’t shaped solely by domestic regulators. Various global frameworks set the tone for how startups operate and raise capital.

The Financial Action Task Force (FATF) is the anchor. Its Travel Rule mandates that virtual asset service providers (VASPs) must collect and share sender and recipient details for transactions over USD$1,000.

This has become the baseline for anti-money laundering (AML) controls worldwide. Even countries without direct crypto legislation often align with FATF guidance to avoid grey-listing, which can choke off banking relationships and international partnerships.

In the European Union, the Markets in Crypto-Assets Regulation (MiCA), enacted in 2023, is the world’s first comprehensive crypto framework. MiCA requires stablecoin issuers to maintain fully backed reserves, mandates clear disclosures, and enforces licensing for all crypto asset service providers across the bloc. Many African fintechs seeking EU partnerships are now expected to meet MiCA-level compliance, since its detailed rules have set a de facto standard for due diligence.

Meanwhile, the United States introduced the GENIUS Act (Guiding and Establishing National Infrastructure for US Stablecoins) in July 2025, targeting stablecoins with strict reserve, reporting, and audit requirements. While narrower than MiCA, it signals a shift toward treating stablecoins like systemic financial products.

Together, FATF, MiCA, and the GENIUS Act create a regulatory “gravity field” that African startups can’t ignore. Even in markets with slower domestic crypto adoption, these rules influence investor expectations, dictate correspondent banking policies, and define what “compliance-ready” looks like for fintechs scaling beyond local borders.

Africa’s Regulatory Patchwork

The continent’s crypto regulation isn’t uniform, but a few trendsetters show where things are heading:

Kenya: In July 2025, Kenya’s National Assembly repealed the controversial 3% Digital Asset Tax for a more lenient 10% excise duty on transaction fees. The shift eases the burden on traders but adds reporting complexity for fintechs and service providers, who must now file returns with the tax authority. Kenya is also on the FATF grey list, which subjects its financial ecosystem to heightened scrutiny from international partners.

The Kenyan National Assembly has completed the first reading of the Virtual Asset Service Providers (VASP) Bill, with the second reading underway as of June 2025. Once debated, amended, and enacted, the law will establish a comprehensive regulatory framework for digital assets.

The Central Bank of Kenya (CBK) and Capital Markets Authority (CMA) are designated as licensing bodies, tasked with enforcing cybersecurity, consumer protection, and oversight of virtual asset activities. This legislation positions Kenya to standardize crypto regulation and align with global compliance standards.

Nigeria: Once a hostile environment, Nigeria reopened banking access for crypto exchanges in December 2023 after lifting a two-year ban. The Central Bank of Nigeria now permits banks to serve crypto companies but bars them from trading digital assets directly, enforcing strict KYC, AML, and reporting standards to curb illicit activity.

The Securities and Exchange Commission has also tightened its oversight, introducing a comprehensive licensing framework for exchanges, custodians, and token issuers. Through initiatives like the Accelerated Regulatory Incubation Program, crypto firms are being fast-tracked into compliance, with higher registration fees and stricter governance requirements signaling a shift from outright prohibition to structured oversight.

South Africa: South Africa has emerged as a regulatory leader on the continent, with the FSCA classifying crypto assets as financial products under the FAIS Act in 2022. By mid-2024, over 130 licenses had been issued to crypto service providers, and dozens of investigations were launched to weed out unlicensed operators.

The licensing framework is deliberately rigorous, pushing firms to strengthen governance, security, and AML capabilities, resulting in some applicants withdrawing altogether. This high bar has legitimized South Africa’s market, attracting institutional players like VALR and spurring innovation, including stablecoin products from major banks.

While gaps remain, such as limited regulation for NFTs and stablecoins, ongoing reforms under the upcoming COFI Bill are expected to create a fully harmonized regime, cementing South Africa’s role as a testing ground for crypto’s institutional future in Africa.

This patchwork means a pan-African crypto strategy isn’t as simple as scaling one compliance framework. Fintechs must design controls that meet FATF’s global bar while adapting to local specifics.

Why Compliance Is the Cost of Growth

For years, African fintechs operated in a regulatory grey zone where crypto innovation outpaced oversight. That window is closing fast, with these three trends shaping the compliance landscape:

1. The Travel Rule Era

The Travel Rule is no longer optional, considering European and Asian exchanges already demand sender and receiver information on every crypto transfer. African fintechs that ignore this will see transactions delayed, blocked, or rejected entirely.

Implementing Travel Rule solutions is now part of basic operational procedures.

2. Stablecoins Under Scrutiny

Stablecoins power everything from remittances to e-commerce, but regulators are watching their reserve quality and custody arrangements closely. Under MiCA, issuers must provide proof of reserves, which means fintechs relying on stablecoins will face similar questions from banking partners and auditors.

The GENIUS Act requires stablecoin issuers to maintain full 1:1 backing with U.S. dollars or Treasury securities, held entirely in U.S. reserves. For emerging markets plugged into the U.S. financial system, this sets a higher standard of trust and liquidity, paving the way for smoother, lower-risk cross-border settlements and remittances.

3. Bank De-risking

Countries like Kenya, South Africa, Nigeria, and Namibia being on the FATF’s grey list means banks in Europe or the U.S. treat transactions involving these jurisdictions as higher risk. That leads to extra due diligence, slower settlements, and in some cases, outright rejection of transactions.

For fintech founders, this isn’t just a compliance exercise; it’s a market access strategy. Without strong controls, scaling internationally becomes nearly impossible.

Building Trust Through Compliance

The upside of compliance is credibility. For African fintechs, a robust compliance program signals to investors, regulators, and customers that your business is built to last.

Key pillars include:

- Crypto-Specific Risk Assessments: Regulators now expect detailed assessments of blockchain-specific risks like mixer exposure (funds with unclear origins), DeFi protocols, and self-hosted wallets.

- Blockchain Analytics: Tools like Chainalysis and Elliptic are no longer optional. They help trace funds, identify risky wallets, and build auditable case files.

- Custody Assurance: Whether self-custodying or using a third-party custodian, fintechs need proof of segregation, secure key management, and frequent reconciliations.

- Market-Specific Tax Compliance: With Kenya’s tax pivot and Nigeria’s evolving FX policies, fintechs need dynamic tax engines to stay compliant.

Think of these controls as part of your product infrastructure, instead of red tape. They’re what will get you a seat at the table with global banks and payment networks.

Shifting the Narrative from Risk to Opportunity

Crypto compliance in Africa isn’t just about avoiding penalties. It’s about unlocking access to deeper liquidity pools, cheaper capital, and cross-border partnerships.

Using South Africa’s licensing regime as an example, by December 2024, 75 companies had obtained CASP licenses. That milestone turned South Africa into a regional crypto hub, attracting institutional interest. Nigeria’s U-turn on bank restrictions signals similar momentum.

Investors are also paying attention. Venture firms increasingly see regulatory readiness as a proxy for operational maturity. Startups with strong compliance programs often secure better valuations and smoother exits.

Lessons From Other Markets

Africa is not the first frontier market to wrestle with crypto oversight. In Latin America, exchanges that embraced compliance early, like Brazil’s Mercado Bitcoin, secured dominant market share once rules tightened.

The same pattern is playing out in Asia, with MiCA-style frameworks spreading quickly. In perspective, Singapore’s Payment Services Act (PSA) and Hong Kong’s Stablecoin Bill both require stablecoin issuers to maintain fully backed reserves and operate under strict licensing regimes.

For African fintechs, this is a blueprint to treat compliance as a safeguard. Those who wait risk being shut out of partnerships and markets.

What’s Next for African Crypto Regulation

Expect three shifts over the next 24 months:

- Unified Standards: More African countries will harmonize rules with FATF guidance, focusing on Travel Rule implementation and VASP licensing.

- Bank Partnerships: With regulations clearer, banks will cautiously re-enter crypto partnerships, especially around remittances and B2B payments.

- Retail Consumer Protection: Regulators will increasingly scrutinize how crypto products are marketed, with penalties for misleading disclosures or predatory fees.

However, these regulatory shifts won’t happen in a vacuum. With several African nations still stuck on the FATF grey list, the continent is under the microscope. The next two years will separate the trailblazers from the underperformers. Those who tighten AML controls and embrace global standards will unlock capital, partnerships, and credibility, while those who stall risk financial isolation

YoguPay’s Take

At YoguPay, we view regulatory shifts not as obstacles, but as catalysts for a stronger, more resilient digital payments ecosystem in Africa. Clearer frameworks level the playing field, rewarding fintechs that invest in compliance early.

What sets YoguPay apart:

- Built-in compliance: Every transaction incorporates FATF-aligned KYC/AML protocols and Travel Rule readiness.

-

- Trusted partnerships: We collaborate with regulated financial institutions to deliver faster, more reliable settlement channels.

-

- User-first security: Transparent pricing, responsible product messaging, and robust fraud prevention ensure our users transact with confidence.

For us, staying ahead means designing solutions that meet today’s evolving standards, so our partners can scale seamlessly and confidently tomorrow.

The Bottom Line

African fintechs are sitting on one of the most transformative growth opportunities in the world: leveraging blockchain rails to fix a fragmented, expensive payments environment. But the price of admission is high. Regulators are no longer looking the other way, and compliance failures could mean losing access to banks, investors, and customers.

By adopting global best practices early, African fintechs can position themselves not just to survive regulation, but to thrive because of it. The companies that get this right will own the next chapter of Africa’s digital finance story.

At YoguPay, our excellence doesn’t stop at being compliance-first. We’re constantly tracking regulatory shifts to help fintechs anticipate changes, stay ahead of risks, and scale confidently in a fast-moving market.