Digital assets have become a structural feature of Africa’s financial ecosystem, prompting regulators to confront a central policy challenge: how to provide legal certainty and systemic safeguards without stifling innovation. Kenya’s Virtual Asset Service Providers (VASP) Act, 2025 marks a significant policy inflection point in this debate. Rather than treating digital assets as a peripheral risk, the Act formally integrates virtual asset activity into the country’s financial regulatory architecture.

Kenya’s framework reflects a broader continental shift toward rules-based oversight aligned with global standards, particularly in areas such as licensing, consumer protection, and anti-money laundering controls. As other African markets accelerate their own regulatory efforts; most notably Ghana with its 2025 VASP legislation, Kenya’s approach offers valuable lessons on institutional design, supervisory coordination, and phased implementation.

This article examines Kenya’s VASP Act in context, compares it with Ghana’s emerging framework, and distills policy insights relevant to regulators shaping sustainable digital asset markets across Africa.

Why Kenya Moved to a VASP Regulatory Framework

For much of the past decade, Kenya has been a leading hub for financial innovation in Africa, first with mobile money via M-Pesa, and more recently with growing adoption of cryptocurrencies and digital assets. According to Chainalysis data, Kenyan users have been among the most active in the world in certain digital asset categories, particularly stablecoins used in cross-border remittances and online commerce.

This rapid uptake presented both opportunity and risk. While digital assets have lowered barriers for payments, remittances, and investment, they have also operated largely outside clear supervisory frameworks. This created vulnerabilities to financial crime, market abuse, and consumer harm, and drew attention from international standard-setting bodies such as the Financial Action Task Force (FATF).

Against this backdrop, the Virtual Asset Service Providers Act, 2025 was enacted and came into force on 4 November 2025.

Key Features of Kenya’s VASP Act

Clear Definitions and Scope

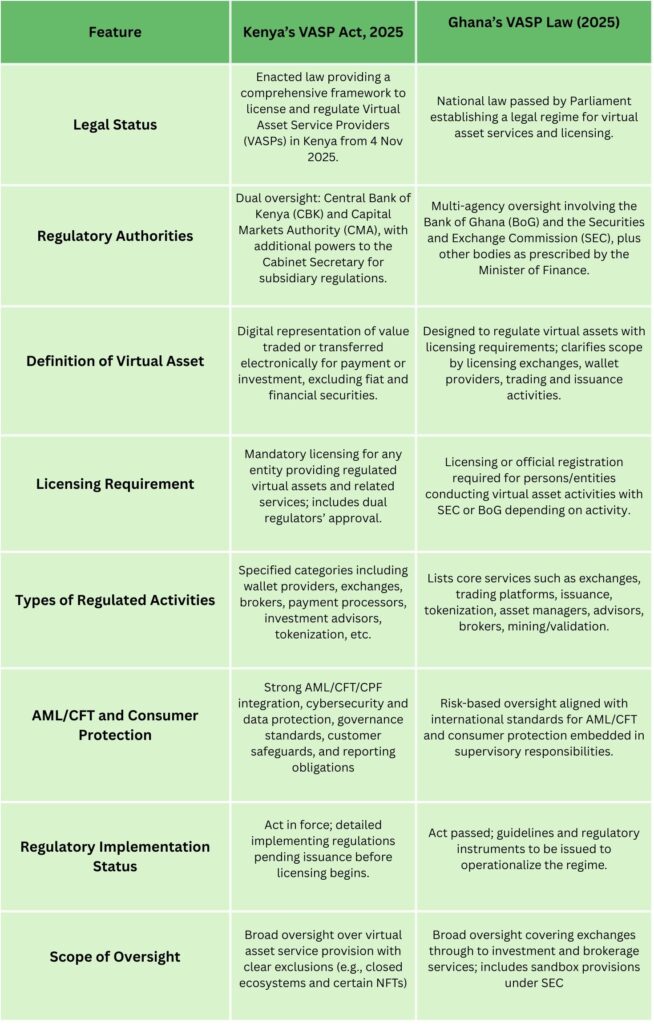

The Kenyan VASP Act defines a “virtual asset” as a digital representation of value that can be traded or transferred electronically and used for payment or investment purposes, while explicitly excluding digital representations of fiat currencies and other traditional financial assets.

This definitional clarity matters: it ensures that only appropriate digital asset activities are captured, reducing regulatory ambiguity and preventing overreach. For example:

- Closed-loop digital tokens with no external tradability are excluded.

-

- NFTs not used for payments or investment are excluded.

The lesson for other African markets is to have a precise statutory definition of “virtual asset,” to reduce uncertainty for market participants and regulators alike.

Dual Regulatory Architecture

Rather than creating a new regulator, Kenya’s framework wisely builds on existing institutions. The Act designates the Central Bank of Kenya (CBK) and the Capital Markets Authority (CMA) as the primary supervisors, with responsibilities structured around the nature of the service being provided.

This division leverages existing regulatory expertise: CBK for payment systems and settlement, and CMA for capital markets and investment-related services. A dual architecture like this can reduce regulatory fragmentation, a lesson that other markets with established institutional capacity should consider.

Licensing and Compliance Framework

Under the Act, every business conducting regulated virtual asset services must obtain a license from the appropriate authority.

Licensing prerequisites include:

- Established corporate structure.

-

- Adequate capital reserves and operational robustness.

-

- Governance frameworks and risk-management systems.

-

- Compliance with cybersecurity and data protection standards.

The Act’s requirements are principles-based, which means regulators have flexibility to adapt rules over time, but it also places the burden on providers to demonstrate strong governance. Other jurisdictions should note that a balance between flexibility and clarity promotes innovation without sacrificing safety.

Financial Crime Controls

A fundamental pillar of the VASP Act is its alignment with regulations against financial crimes such as; anti-money laundering (AML), countering financing of terrorism (CFT), and countering proliferation financing (CPF) standards. VASPs must implement Know-Your-Customer (KYC) procedures, transaction monitoring, suspicious activity reporting, and sanctions screening.

For African markets confronting similar digital asset growth, embedding AML/CFT/CPF obligations directly into a VASP statute enhances legitimacy and reduces regulatory risk.

Consumer Protection and Market Integrity

The Act obliges VASPs to:

- Safeguard client assets.

-

- Maintain segregated accounts.

-

- Ensure transparent disclosures and fair marketing.

-

- Implement business continuity and disaster recovery plans.

These protective measures are crucial to building investor confidence and supporting sustainable ecosystem growth.

Structural and Market Implications

A Phased Implementation

Although the VASP Act is in force, regulators in Kenya have not yet begun issuing licenses because detailed regulations are still under development. This reflects a broader reality: framework enactment does not automatically equal market readiness.

Licensing regimes must be supported by:

- Comprehensive rulebooks

-

- Regulatory capacity building

-

- Clear timelines for compliance

Other African markets should similarly anticipate a phased rollout rather than immediate market activation.

Impact on Innovation and Capital Flows

By codifying digital asset service activities, Kenya has:

- Reduced uncertainty for entrepreneurs and investors.

-

- Elevated the country’s attractiveness as a regional hub for digital finance.

-

- Clarified pathways for foreign participation while maintaining supervisory oversight.

This kind of clarity can help retain innovative local talent while attracting global firms that seek regulated environments. Digital asset investors can take proactive steps to prepare for regulatory adoption, smoothing the shift from fragmented or informal controls to comprehensive supervisory oversight.

Integrating Infrastructure Providers: API, Cross-Border Settlement, and WaaS

A core pillar in any digital-asset ecosystem is the infrastructure that enables connectivity between traditional financial systems and blockchain-based services. This is where cross-border payment API providers, and Wallet-as-a-Service (WaaS) platforms like YoguPay play a critical role.

The Role of API Infrastructure Providers

In regulated environments, seamless application programming interfaces (APIs) enable licensed VASPs to interact with banks, payment processors, and regulatory reporting systems. Business payment APIs in Africa ensure:

- Real-time compliance checks

-

- Automated settlement messaging

-

- Integration with traditional banking rails

For example, licensed Kenyan exchanges and custodial services will require robust multi-currency API connectivity to local bank settlement networks, since a well-regulated API layer reduces operational risk and strengthens regulatory reporting.

Payment infrastructure providers like YoguPay, which offer modular APIs that abstract complexity, empower VASPs and fintechs to deploy wallets, payments, and settlement capabilities without building from scratch.

These services also help VASPs meet regulatory requirements around custody and asset safekeeping, necessitating business cross-border payments in Africa.

Cross-Border Settlement and Compliance

Digital assets are inherently borderless. This makes cross-border settlement infrastructure essential, especially in African markets where remittances and regional trade are significant. Clearing and settlement infrastructure must be built with compliance at the forefront, ensuring:

- Cross-border AML/CFT alignments

-

- Currency conversion compliance

-

- Settlement finality across jurisdictions

Infrastructure providers that deliver compliance-ready settlement layers reduce the operational and regulatory burden on digital asset operators, allowing them to avoid duplicative compliance build-outs and accelerate market entry. In this context, VASPs can leverage cross-border settlement enabling platforms such as YoguPay to access compliant, scalable, and reliable remittance rails aligned with emerging regulatory requirements.

Wallet-as-a-Service (WaaS)

Custodial and non-custodial wallet services require advanced security, key management, and user-experience capabilities. WaaS platforms like YoguPay provide regulatory-aligned wallet infrastructure that can be embedded into fintech applications. Such providers deliver:

- Secure storage and key management

-

- Integration with licensing requirements for custodial assets

-

- Dynamic AML/CFT and KYC modules

This approach democratizes the ability for new entrants to meet compliance standards without heavy upfront technology investments.

Curious how regulated stablecoins could fit into your operational workflow? Connect with a YoguPay representative to explore use cases and regulatory considerations.

Comparative Insight: Ghana’s VASP Act 2025

While Kenya’s VASP Act took effect in late 2025 and is awaiting detailed regulations, Ghana followed a similar but distinct path in its approach to digital asset regulation.

Ghana’s Regulatory Developments

Ghana’s Parliament passed its own Virtual Asset Service Providers Bill (VASPs) in December 2025, and President Mahama signed it into law by year-end. It formally legalizes cryptocurrency trading and establishes a regulatory oversight framework.

Key elements of Ghana’s law include:

- A clear legal foundation recognizing and regulating digital asset activities.

-

- Mandatory licensing or registration of VASPs with the Bank of Ghana (BoG) or the Securities and Exchange Commission (SEC), depending on activity type.

-

- Requirements for cybersecurity, AML/CFT controls, and consumer protection aligned with global standards.

-

- The law positions Ghana among the first West African nations to regulate digital assets comprehensively.

Unlike Kenya’s dual-supervisor model where oversight is split, Ghana’s VASP law often focuses regulatory responsibility between the central bank and securities regulator, similar in spirit but not necessarily identical in structure.

Lessons from Ghana’s Approach

Comparing Ghana and Kenya yields several instructive insights:

- Legal Recognition Before Regulation: Ghana’s law explicitly legalizes cryptocurrency trading, reducing regulatory ambiguity for market participants from day one. In Kenya, the VASP Act regulates providers but does not inherently confer legal tender status for digital assets, which may slow mainstream adoption initially.

-

- Dual Regulatory Roles: Both countries allocate regulatory responsibilities based on service type, but Ghana’s approach is more centrally anchored with clear supervisory roles for BoG and SEC. This highlights that there is no single “correct” model; regulators should be assigned based on existing institutional expertise.

-

- Operational Readiness: Both jurisdictions now face the practical challenge of drafting detailed regulations and building supervisory capacity. Kenya’s phased implementation approach reflects cautious calibration; Ghana’s model anticipates a rapid roll-out of directives in early 2026.

-

- Global Standards Alignment: Both frameworks echo global best practices, like FATF recommendations, by embedding AML/CFT obligations and consumer protection. This underscores the importance of regulatory alignment in cross-border digital finance.

Kenya and Ghana: A Comparative Look at Crypto Laws

Policy Lessons for African Markets Building Digital Asset Frameworks

Drawing on Kenya and Ghana, here are practical lessons for other African markets exploring digital asset regulation:

Define Digital Assets Clearly

Ambiguous definitions lead to regulatory uncertainty; hence, Kenya’s approach of excluding closed-loop tokens and central-bank digital currencies helps narrow focus and reduce over-regulation.

Allocate Regulatory Responsibilities Based on Expertise

Rather than creating new standalone regulators, leverage existing institutions with complementary mandates; such as payments regulators (central banks) and capital market authorities.

Ghana also applies a similar dual-oversight framework, with the Bank of Ghana (BoG) and the Securities and Exchange Commission (SEC) regulating issuance, storage, and transfer of digital assets.

Embed AML/CFT/CPF and Consumer Protection from Day One

Digital assets are attractive to fraudsters and money launderers. Therefore, legislating compliance obligations early conveys seriousness and builds trust.

Anticipate a Phased Implementation

Licensing requirements should be accompanied by detailed regulations, supervisory training, and clear timelines. Fragmentary or rushed implementation can create uncertainty.

Facilitate Innovation Through Regulatory Sandboxes

Regulated sandboxes and tiered licensing can allow new models to be tested under supervision without compromising safety.

Programmable wallet providers, such as YoguPay, increasingly embed regulatory sandbox environments within their platforms, enabling fintechs and payment service providers to experiment with digital asset use cases under defined compliance controls.

By abstracting regulatory complexity at the infrastructure layer, these providers allow market participants to innovate without independently building compliance and supervisory frameworks. As regulatory regimes mature, supervisors and licensed entities alike can integrate with these compliance-first rails, creating a scalable pathway for broader digital asset adoption within formal financial systems.

Reduce operational risk in cross-border payments and wallet management with ease. Connect with a YoguPay advisor to learn how to move money safely and efficiently.

The Role of Fintech Infrastructure in a Regulated Digital Asset Economy

In a regulated landscape, the ecosystem flourishes not just with licensed exchanges or custodians, but with robust infrastructure that ensures interoperability, compliance, and operational resilience.

APIs and Regulatory Reporting

APIs serve as the backbone for compliance automation. They enable regulators to receive real-time transaction data and help VASPs comply with reporting obligations. Infrastructure providers that embed compliance modules into their APIs reduce friction for regulated entities.

Cross-Border Settlement Networks

Digital asset ecosystems thrive on efficient cross-border settlement. In Africa, where remittances constitute meaningful economic flows, infrastructure that supports settlement with compliance guardrails is a strategic advantage. Infrastructure providers that integrate with multiple fiat and digital systems can expand reach quickly.

WaaS Platforms

Wallet-as-a-Service platforms provide licensed digital asset investors with ready-built, secure wallet infrastructure. This is invaluable in regulated contexts where custodial integrity, key management, and AML/KYC integration are statutory requirements.

WaaS providers like YoguPay bridge technological complexity and compliance, enabling fintechs to focus on user experience and product innovation.

Conclusion: A Roadmap for Sustainable Digital Asset Markets

Kenya’s Virtual Asset Service Providers Act, 2025 is a pioneering statute in African digital finance. Its blend of clear definitions, structured oversight, compliance mandates, and phased implementation offers valuable lessons for other markets.

When viewed alongside Ghana’s newly enacted framework, it becomes evident that the future of regulated digital asset markets in Africa rests on clarity, institutional alignment, and infrastructure enablement. For regulators and market participants alike, this is a message to regulate with precision, innovate with purpose, and build with resilient infrastructure.

Strategic partnerships with API, settlement, and integrated wallet providers like YoguPay can accelerate compliant market entry, support cross-border flows, and unlock the transformative potential of digital assets across the continent.

Ready to upgrade your payments infrastructure and run compliant cross-border transactions with confidence? Speak with YoguPay for a tailored walkthrough on compliance, risk management, and scaling global payments.